All Categories

Featured

Table of Contents

Note, however, that this does not say anything concerning readjusting for inflation. On the bonus side, also if you assume your choice would be to purchase the securities market for those seven years, and that you 'd get a 10 percent yearly return (which is much from particular, specifically in the coming years), this $8208 a year would certainly be more than 4 percent of the resulting small stock value.

Example of a single-premium deferred annuity (with a 25-year deferment), with 4 repayment choices. The month-to-month payment below is greatest for the "joint-life-only" choice, at $1258 (164 percent greater than with the immediate annuity).

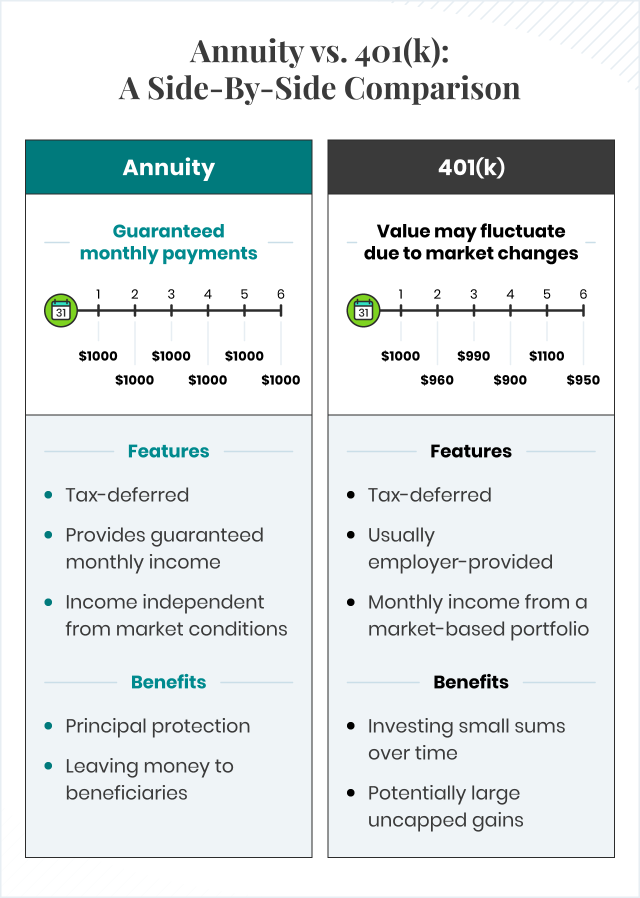

The way you purchase the annuity will figure out the response to that concern. If you purchase an annuity with pre-tax dollars, your costs decreases your taxed income for that year. Ultimate payments (regular monthly and/or lump sum) are exhausted as routine earnings in the year they're paid. The benefit below is that the annuity may let you postpone tax obligations beyond the internal revenue service payment limitations on IRAs and 401(k) plans.

According to , getting an annuity inside a Roth plan causes tax-free repayments. Buying an annuity with after-tax bucks outside of a Roth leads to paying no tax obligation on the section of each payment credited to the initial costs(s), but the continuing to be part is taxable. If you're establishing up an annuity that begins paying prior to you're 59 years old, you might have to pay 10 percent very early withdrawal penalties to the IRS.

Can I get an Fixed Annuities online?

The expert's very first step was to establish an extensive monetary prepare for you, and after that discuss (a) just how the proposed annuity suits your general strategy, (b) what options s/he thought about, and (c) just how such options would or would not have actually led to lower or higher payment for the consultant, and (d) why the annuity is the premium choice for you. - Lifetime payout annuities

Naturally, a consultant may try pressing annuities also if they're not the very best suitable for your circumstance and objectives. The reason could be as benign as it is the only product they market, so they drop target to the proverbial, "If all you have in your toolbox is a hammer, rather quickly whatever starts appearing like a nail." While the expert in this circumstance may not be unethical, it boosts the threat that an annuity is a bad choice for you.

How do I choose the right Lifetime Payout Annuities for my needs?

Since annuities usually pay the representative offering them much higher payments than what s/he would certainly receive for investing your cash in common funds - Fixed vs variable annuities, not to mention the absolutely no commissions s/he 'd get if you buy no-load common funds, there is a huge motivation for agents to press annuities, and the much more complicated the much better ()

A dishonest consultant suggests rolling that quantity right into brand-new "much better" funds that simply occur to bring a 4 percent sales load. Consent to this, and the expert pockets $20,000 of your $500,000, and the funds aren't most likely to do far better (unless you selected even extra poorly to start with). In the same example, the advisor could guide you to purchase a complex annuity keeping that $500,000, one that pays him or her an 8 percent compensation.

The consultant tries to hurry your choice, declaring the deal will certainly quickly disappear. It may undoubtedly, however there will likely be comparable offers later. The expert hasn't identified just how annuity payments will be taxed. The consultant hasn't revealed his/her settlement and/or the charges you'll be billed and/or hasn't shown you the influence of those on your ultimate payments, and/or the settlement and/or costs are unacceptably high.

Your family background and present health indicate a lower-than-average life expectancy (Income protection annuities). Present rate of interest, and hence projected settlements, are historically reduced. Even if an annuity is appropriate for you, do your due persistance in comparing annuities offered by brokers vs. no-load ones marketed by the releasing business. The latter may require you to do even more of your own research study, or utilize a fee-based economic consultant that may get compensation for sending you to the annuity company, but may not be paid a greater payment than for other financial investment options.

Who should consider buying an Annuity Interest Rates?

The stream of monthly repayments from Social Safety and security is comparable to those of a postponed annuity. Because annuities are volunteer, the people purchasing them generally self-select as having a longer-than-average life expectations.

Social Protection benefits are fully indexed to the CPI, while annuities either have no rising cost of living defense or at most offer an established percentage yearly boost that might or may not make up for inflation completely. This type of biker, just like anything else that raises the insurance provider's threat, needs you to pay more for the annuity, or accept lower payments.

What types of Retirement Annuities are available?

Please note: This short article is planned for informative objectives only, and need to not be considered economic recommendations. You ought to seek advice from a monetary specialist before making any major monetary decisions. My job has had several unforeseeable spins and turns. A MSc in academic physics, PhD in speculative high-energy physics, postdoc in fragment detector R&D, study position in experimental cosmic-ray physics (consisting of a number of sees to Antarctica), a quick stint at a little engineering solutions business supporting NASA, followed by beginning my own little consulting technique sustaining NASA projects and programs.

Since annuities are intended for retirement, taxes and penalties might use. Principal Defense of Fixed Annuities.

Immediate annuities. Deferred annuities: For those who desire to expand their cash over time, but are willing to delay accessibility to the money until retired life years.

Lifetime Income Annuities

Variable annuities: Offers better possibility for growth by investing your money in financial investment alternatives you select and the capacity to rebalance your portfolio based on your preferences and in such a way that aligns with altering economic goals. With taken care of annuities, the company spends the funds and gives a rate of interest to the customer.

:max_bytes(150000):strip_icc()/present-value-annuity.asp-Final-7d2ae860c2b044069d77d5e626c5a6f3-72cf6d2c9f9041608b7cd343cbc3f2f4.png)

When a death insurance claim occurs with an annuity, it is essential to have a named recipient in the agreement. Different choices exist for annuity survivor benefit, depending on the agreement and insurance firm. Picking a refund or "duration particular" choice in your annuity gives a survivor benefit if you die early.

Annuities

Naming a recipient various other than the estate can help this process go much more smoothly, and can aid guarantee that the proceeds go to whoever the private desired the money to go to rather than going through probate. When present, a fatality advantage is automatically consisted of with your agreement.

{kind=link}

Latest Posts

What should I know before buying an Fixed Indexed Annuities?

Where can I buy affordable Annuity Accumulation Phase?

What is included in an Annuity Contracts contract?